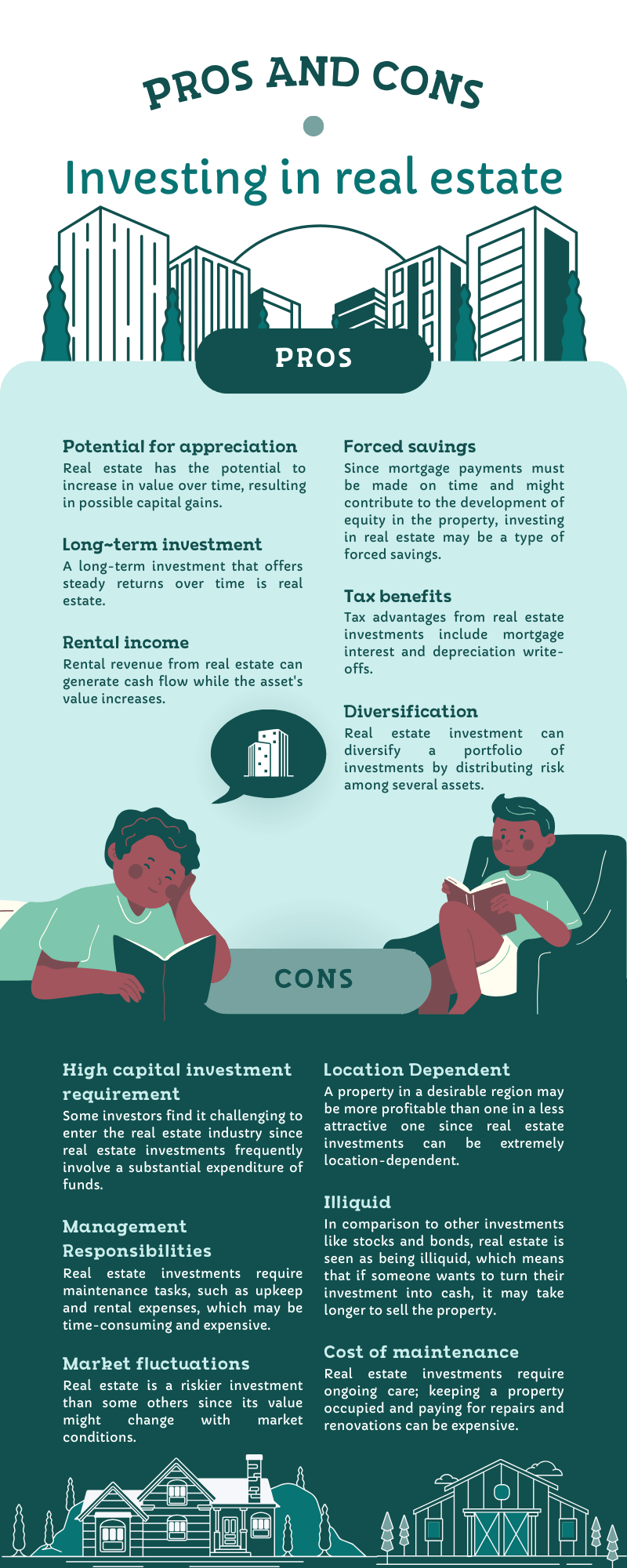

Have you ever imagined yourself as a savvy real estate investor, harnessing the power of the market to build significant wealth over time? The good news is, with smart mortgage strategies tailored for the Canadian market, this doesn’t just have to be a daydream. Real estate has long stood as a cornerstone of wealth building, and by leveraging the right mortgage approaches, you could unlock the door to financial prosperity and security. In this guide, we’ll walk through the pivotal steps and strategies that every Canadian real estate investor should know to turn properties into profitable investments.

Understanding the Real Estate Market:

Assessing Market Conditions for Investment

Before signing any mortgage papers, it’s crucial to have your finger on the pulse of the Canadian real estate market. This means understanding which areas are ripe for investment, recognizing the trends in housing demands, and knowing the economic factors that affect property values. A thorough market analysis can pinpoint where the next hot spot might be—be it the bustling urban centers of Toronto and Vancouver or the steadily growing suburban areas like those around Halifax or Kelowna.

Mortgage Options for Investors:

Choosing the Right Mortgage for Your Investment Strategy

The Canadian mortgage landscape offers various options, each with its own set of benefits and considerations. For instance, fixed-rate mortgages can offer the security of consistent payments throughout the term, which is excellent for planning your cash flow. On the other hand, adjustable-rate mortgages might start lower, providing initial savings that could be redirected into property improvements or other investments.

Leverage and Cash Flow Considerations:

Balancing Leverage and Liquidity in Real Estate Investments

In real estate, leverage can be your best friend or your worst enemy. It’s the art of using borrowed capital—like mortgages—to increase the potential return of an investment. In Canada, the rules around leverage are stringent, but with the right approach, you can use it to your advantage without overextending your financial reach. Keeping a keen eye on cash flow is also paramount to ensure you’re not caught off-guard by market fluctuations or unexpected expenses.

The Role of Credit in Real Estate Investment:

Optimizing Your Credit Profile for Better Loan Terms

Your credit score is like your financial handshake—it tells lenders a lot about you at a glance. In Canada, a strong credit score can unlock better mortgage rates and terms, directly impacting the profitability of your investment. Building and maintaining good credit is not just about paying bills on time; it’s also about understanding how credit utilization and credit history work.

Down Payment Strategies:

Navigating Down Payments for Maximum ROI

The size of your down payment can greatly influence the returns on your investment property. In Canada, the minimum down payment is a sliding scale depending on the property price, but going beyond the minimum can lower your mortgage payments and interest costs. Creative strategies, like partnering with other investors or tapping into a home equity line of credit, can provide the funds necessary for a more substantial down payment without depleting your reserves.

Tax Implications and Benefits:

Mortgage Tax Considerations for Real Estate Investors

Tax considerations play a critical role in the profitability of Canadian real estate investments. Mortgage interest on investment properties is tax-deductible, which can lead to significant tax advantages. However, navigating the complexities of the Canadian tax system requires a strategic approach to ensure you’re maximizing these benefits while remaining compliant.

Refinancing as a Growth Tool:

When and How to Refinance for Investment Expansion

Refinancing can be a strategic maneuver for growth-minded investors in Canada. It involves revising the interest rate, payment schedule, and terms of the existing mortgage, potentially freeing up capital for additional investments. The key is timing—refinancing when interest rates are low can reduce your payments and increase cash flow.

Risk Management:

Mitigating Financial Risks in Mortgage Strategies

Any investment includes a degree of risk, and real estate is no exception. Risk management strategies are vital, from having adequate insurance coverage to creating contingency funds for unforeseen circumstances. Thorough due diligence for every potential investment can mitigate risks and protect your portfolio from volatility in the Canadian market.

Building a Team of Experts:

The Importance of Professional Guidance

No real estate investor is an island, especially in the complex Canadian property market. Building a team of experts—including a knowledgeable mortgage broker, a savvy real estate lawyer, and a financial advisor who understands the intricacies of real estate investing—can be one of your smartest moves. They can offer tailored advice and ensure that your investment decisions are informed and strategic.

Smart mortgage strategies are more than just finding a loan with the best rate; they’re about crafting a comprehensive approach that considers market conditions, leverage, cash flow, credit, and tax implications. For real estate investors in Canada, these strategies form the bedrock of a wealth-building plan that can lead to long-term prosperity.

Are you ready to harness these mortgage strategies in your real estate investment journey? Perhaps you’ve already seen success and have insights to share? Comment below with your experiences or reach out to our expert team for personalized advice. Let’s build wealth together.

Glossary:

Adjustable-Rate Mortgage (ARM): A type of mortgage loan where the interest rate adjusts over time based on an index.

Cash Flow: The net amount of cash and cash equivalents being transferred into and out of a business, or in this context, an investment property.

Credit Score: A numerical expression based on a level analysis of a person’s credit files, to represent the creditworthiness of an individual.

Down Payment: An initial payment made when something is bought on credit.

Equity: The value of an owner’s interest in real estate over and above the liabilities against it.

Fixed-Rate Mortgage: A mortgage that has a fixed interest rate for the entire term of the loan.

Interest-Only Mortgage: A type of mortgage where the borrower only pays the interest on the loan for a set period.

Leverage: The use of various financial instruments or borrowed capital to increase the potential return of an investment.

Liquidity: The ease with which an asset, or security, can be converted into ready cash without affecting its market price.

Mortgage Refinancing: The process of replacing an existing mortgage with a new one, typically with different terms.

Return on Investment (ROI): A measure used to evaluate the efficiency of an investment.

Tax Deduction: A reduction of income that is able to be taxed, often due to expenses, particularly those incurred to produce additional income.

Frequently Asked Questions

What is the minimum down payment for investment properties in Canada?

The minimum down payment in Canada is generally 20% for investment properties that are not owner-occupied. However, for properties priced under $500,000, the minimum is 5% for the first $500,000 and 10% for the portion of the price above $500,000.

How does an adjustable-rate mortgage (ARM) work?

An ARM has an interest rate that may change periodically depending on changes in a corresponding financial index that’s associated with the loan. Typically, this means your payments can increase or decrease.

Why is my credit score important when applying for a mortgage in Canada?

Your credit score is important because it influences the interest rate you’ll be offered on a mortgage. A higher score can mean lower rates, which can save you thousands of dollars over the life of your loan.

Can I deduct mortgage interest from my Canadian investment property on my taxes?

Yes, mortgage interest on investment properties is generally deductible on your Canadian tax return, but it must be associated with the income the property generates.

Is it better to have a fixed-rate or adjustable-rate mortgage for my investment property?

It depends on your financial situation and investment strategy. A fixed-rate mortgage offers stability with consistent payments, while an ARM might offer lower initial payments. You should consult with a financial advisor to decide which is best for your specific circumstances.

How often can I refinance my investment property?

You can refinance as often as it makes financial sense and as permitted by your lender’s terms. However, each refinance comes with costs, so it’s important to weigh these against the potential benefits.

What should I consider before refinancing my investment property?

Before refinancing, consider the break-even point, which is when the cost of refinancing is outweighed by the savings from your new loan. Also, consider how long you plan to hold the property and whether the terms of the new loan are favorable.